Table of Content

Lenders use the loan-to-value ratio to determine how much money an investor can borrow. If a borrower has paid down a good deal of their mortgage—or if the home’s value has risen significantly—then the borrower could get a sizable loan. For example, if you owe $150,000 on a home valued at $250,000, you have $100,000 in equity. Assuming that your credit is good, and that you otherwise qualify, you can take out an additional loan using that $100,000 as collateral.

At the end of the draw period, HELOCs enter the repayment period, during which loans are repaid over time. In some cases, homeowners also may have the option of converting their outstanding balance to a fixed-rate loan in order to set level monthly payments. However, funds may not be drawn against a line after the draw period ends. Provided by a mortgage lender, home equity financing allows you to borrow money against the equity in your home.

Loan

They will also likely pull your credit report to review your credit score in order to conclude that you are a low risk borrower. The amount you could get approved for will ultimately be based on the equity you have in your home. In order to validate that, the bank or credit union will often order an appraisal to confirm the value of your home. Tap into your home's built-up equity with a fixed-rate loan or flexible line of credit.

If your home’s value decreases, you might end up owing more than your property is worth. Any opinions, analyses, reviews or recommendations expressed here are those of the author’s alone, and have not been reviewed, approved or otherwise endorsed by any financial institution. This editorial content is not provided by any financial institution. This keeps things simple and can release a great deal of cash very quickly—cash that can even help improve your property's value. Amanda Jackson has expertise in personal finance, investing, and social services. She is a library professional, transcriptionist, editor, and fact-checker.

Is a HELOC a Second Mortgage?

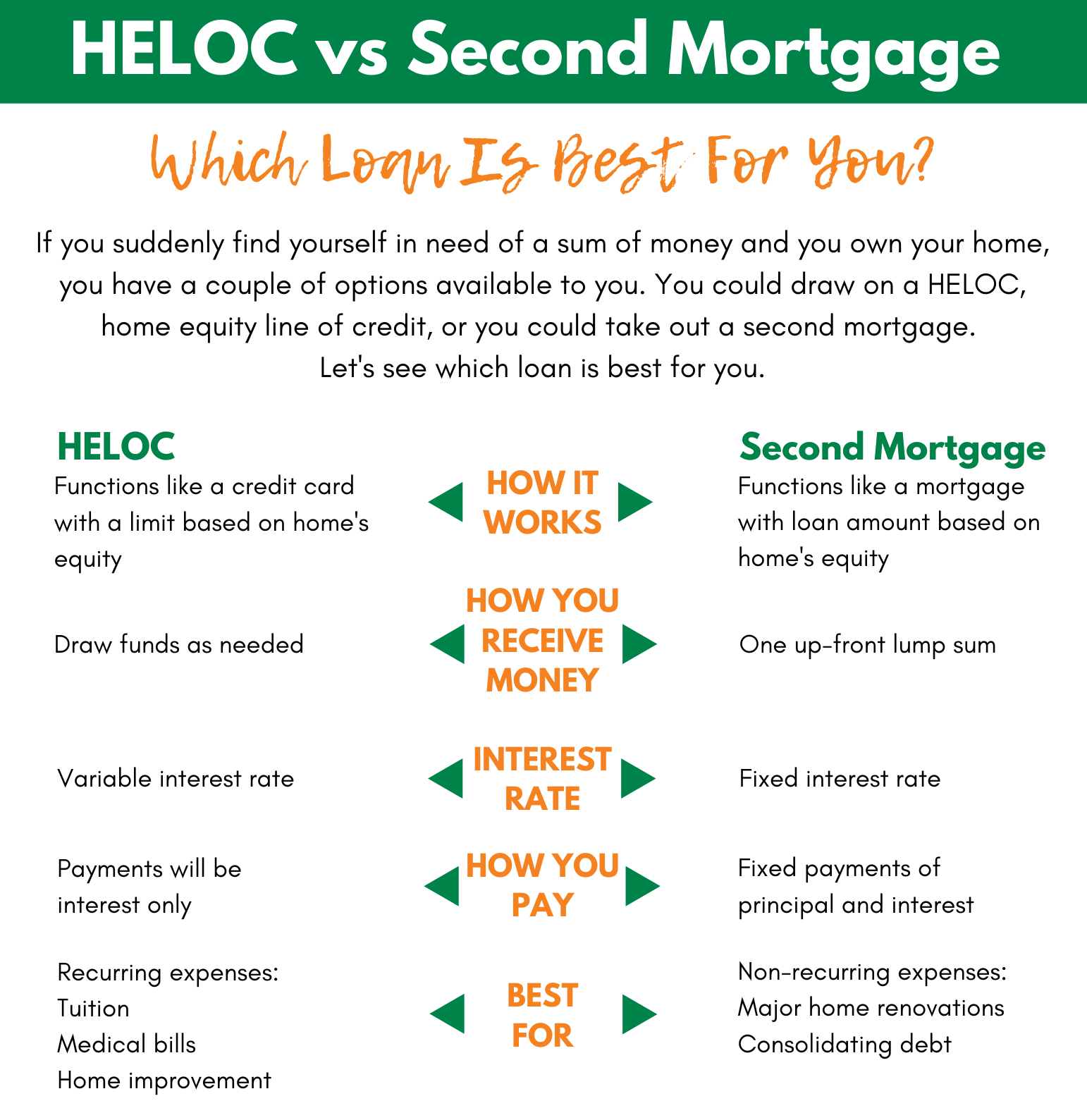

HELOCs give you access to a variable, low-interest-rate credit line that allows you to spend up to a certain limit. HELOCs are a potentially better option for people who want access to a revolving credit line for variable expenses and emergencies that they can’t predict. In the short term, the rate on a loan may be higher than a HELOC, but you are paying for the predictability of a fixed rate. Both home equity loans and HELOCs allow consumers to gain access to funds that they can use for various purposes, including consolidating debt and making home improvements. However, there are distinct differences between home equity loans and HELOCs.

We do anticipate that banks will get a little more conservative on max loan-to-value leverage ratios when they see home values start to plateau. HELOCs can be useful as a home improvement loan because they allow you the flexibility to borrow as much or as little as you need. If it turns out that you need more money, you can get it from your line of credit—assuming there’s still availability—without having to reapply for another mortgage loan. Please avoid using a credit card to fund higher dollar amount needs.

Closing Costs for HELOCs and Home Equity Loans

If you are a high-risk borrower, it may be a good idea to seek out a credit counseling service for advice and assistance before signing up for a high-interest HELOC or home equity loan. However, an equity line of credit is revocable—just like a credit card. If your financial situation worsens or your home’s market value declines, then your lender could decide to lower or close your credit line. So, although the idea behind a HELOC is that you can draw upon the funds as you need them, your ability to access that money isn’t a sure thing.

But if you make repayments on a timely basis, your credit score will recover quickly. Borrowers typically pay only interest during the draw period but can pay down the principal too, although it’s not required. HELOCs are secured loans, meaning that the borrower’s home is used as collateral to secure the loan. Because the home is used as collateral, failure to repay the HELOC could lead to foreclosure.

Key Differences Between Reverse Mortgages, Home Equity Loans, and HELOCs

For buyers who want to get a lot of money for their HELOC and don’t want to deal with high repayment values in the future. Offers 0.25 % interest rate discount for PNC Bank members with automatic payments from qualifying checking accounts. If you'll need a fixed amount of money all at once for a certain purpose (e.g., remodeling the kitchen or paying off other high-interest debts), you might want to take out a home equity loan.

Keep in mind, though, that you’re using your home for collateral, so the lender can foreclose on your property if you default on your payments. In addition to their regular monthly interest payments, a borrower who has drawn money against their line of credit also is able to make payments against their outstanding balance as they’re able. And, as they pay down their outstanding balance, they are able to use their available credit again, just like with a credit card. A home equity line of credit is a loan that uses your house as collateral. It is possible to get approved without meeting these requirements by going through lenders that specialize in high-risk borrowers, but expect to pay much higher interest rates.

For example, if you want a structured loan that will let you know exactly what your monthly payment will be and when your loan will be paid back, then a home equity loan is a great choice. If you prefer a more flexible financing option, or if you aren’t sure how much funding you’ll need or how you’ll use the money, a HELOC offers homeowners much more flexibility. Typically, the term of an equity loan term can be anywhere from five to 30 years, but the length of the term must be approved by the lender. Whatever the period, borrowers will have stable, predictable monthly payments to make for the life of the equity loan. With a home equity loan, you receive the entire loan amount as a lump sum payment with repayment terms set to a fixed interest rate over a specified length of time.

4This HELOC is a variable rate plan as described in the applicable loan documents. The Index is the Prime Rate as published in The Wall Street Journal. Qualification and APR dependent on credit history, debt, loan-to-value, ability to repay, home ownership, and other factors.

You can usually borrow up to 85% of the equity in your home through a home equity loan. You’ve decided to do some home renovations, and you want to access the equity you have in your house. You go to a lender and they hire an appraiser, who sets the value of your home at $220,000. The lender may let you borrow up to $187,000 against the house, minus the $100,000 that you already owe on your first mortgage.

No comments:

Post a Comment